Strait of Hormuz

33 km chokepoint for a fifth of global oil; IRGC drone strikes resumed despite ceasefire.

Last refreshed: 13 July 2026 · Appears in 7 active topics

Record oil flow, then drone strikes: can the ceasefire survive Qeshm?

Timeline for Strait of Hormuz

Blockade turns Hormuz threat to fact

Iran Conflict 2026Trump floats then drops Hormuz toll

Iran Conflict 2026Freight has not confirmed the spike

European Oil MarketsTTF round-trips back above EUR 50

European Energy MarketsMentioned in: 140 US sorties, zero signed paper

Iran Conflict 2026Is the Strait of Hormuz open or closed as of 12 July 2026?

How much of Europe's gas supply depends on the Strait of Hormuz staying open?

What is the connection between Qatari LNG and European gas storage?

Background

After the Islamabad MOU (16 June) and CENTCOM's end to its 66-day naval blockade on 18 June, commercial traffic recovered steadily through late June. By 25 June 2026, Hormuz cleared a single-day record of 20 million barrels in 24 hours, confirmed by US Energy Secretary Chris Wright, approaching the strait's pre-war baseline for the first time since the conflict began.

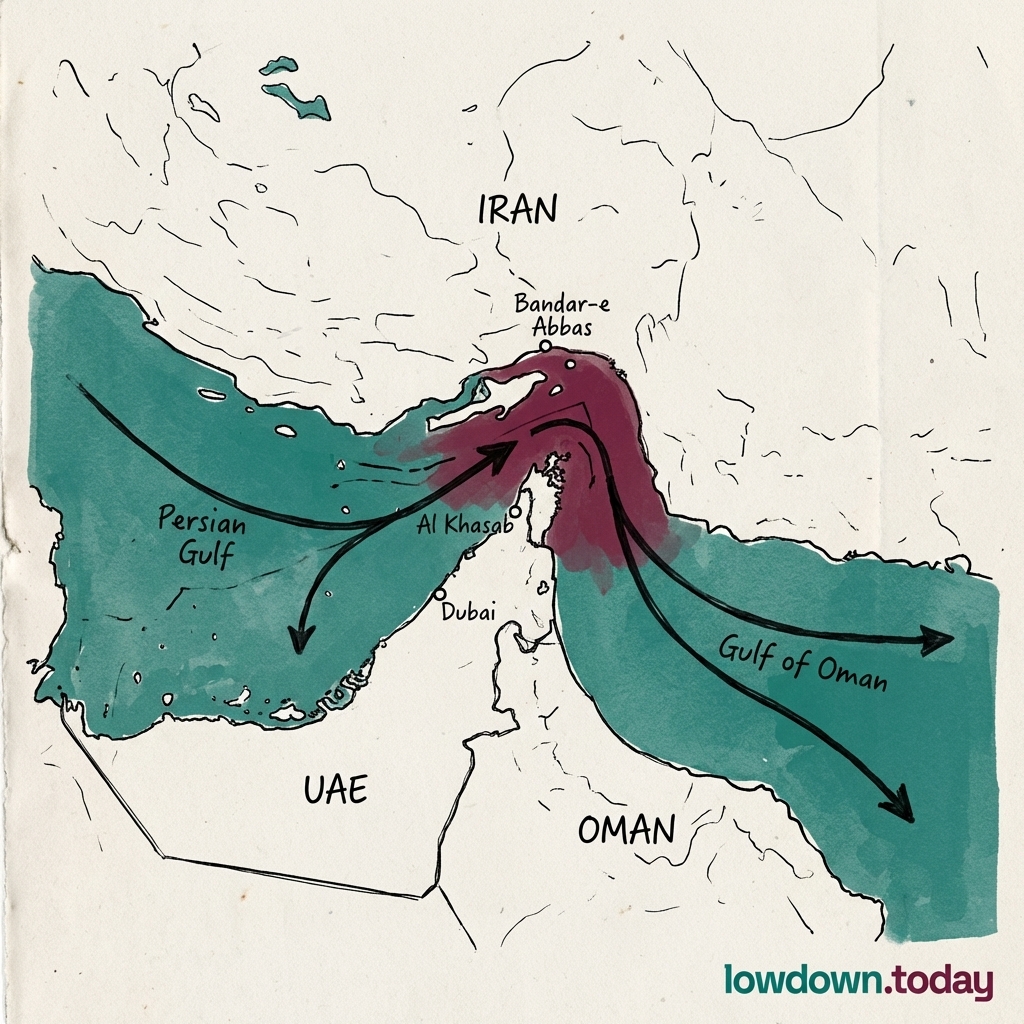

The record held less than 48 hours. IRGC drones struck the Singapore-flagged container vessel Ever Lovely on 25 June inside the Oman-IMO SAFE corridor, then the tanker Kiku on 27 June, both without casualties. The Persian Gulf Strait Authority suspended the corridor after the first strike, leaving an estimated 11,000 seafarers stranded without an exit route. CENTCOM responded on 26 June with airstrikes on Iranian missile and drone storage on Qeshm Island and a coastal radar near Sirik, the first US kinetic strike on Iranian soil since the MOU.

The market's verdict was telling: Brent fell to $71.99 on 26 June, closing through the kinetic exchange and below the pre-conflict floor, pricing the corridor as durable. Three structural barriers from the blockade era persist: London P&I war-risk cover remains withdrawn, the BIMCO CONWARTIME clause keeps Gulf Charter contracts in force, and mine-clearance in navigable channels is incomplete. The MOU reframes the PGSA as a joint Iran-Oman provider under UNCLOS Article 26(2); the Ceasefire's durability after Qeshm is now the paramount test.

By late June, Tehran and CENTCOM reached a 29 June verbal stand-down following the Qeshm/Sirik strikes, but the stand-down did not restore normal traffic. Four days on, IMF PortWatch counted only 27-43 transits a day against an ~84/day pre-crisis baseline, and QatarEnergy's LNG restart ran at roughly 35% of its 77 MTPA nameplate capacity, below the 50%-within-a-month pace it had guided at reopening. Lloyd's List reported the binding constraint was logistics rather than diplomacy: escort convoys can clear only three to four tankers a day through the strait on seven to eight escort warships, a ratio unable to scale without more warships in the corridor.

The dual-status dispute reached a new peak on 12 July 2026. The IRGC Navy struck the Cyprus-flagged container ship GFS Galaxy in the strait and declared it "closed until further notice", with the Persian Gulf Strait Authority posting that passage was "not possible"; one of the vessel's eleven Indian crew was reported missing. CENTCOM answered with its third strike wave of the week, roughly 140 targets against missile batteries, air defence, IRGC fast-attack boats and Qeshm Island, taking the week's total past 300 strikes, and declared the strait open to lawful traffic. Neither side operated under a signed instrument: Washington issued no new Iran authorisation through the exchange, leaving Hormuz's legal status as contested as its physical transit.

The Strait of Hormuz is a 33 km wide chokepoint between Iran to the north and Oman and the UAE to the south, connecting the Persian Gulf to the Gulf of Oman and the Arabian Sea. Before the 2026 conflict, roughly 20 million barrels of crude oil per day and 20% of global LNG passed through it daily, making it the single most consequential maritime chokepoint for global energy. The strait is the sole maritime exit for all Gulf producers (Saudi Arabia, Kuwait, Iraq, UAE, Qatar, and Iran) to world markets.

Since Russian pipeline gas exited the European market in 2022, Qatari LNG shipped through the Strait of Hormuz has become a structural pillar of European winter supply, and the strait's shipping-risk premium now moves European gas prices even when physical European supply is comfortable. On 13 July, TTF front-month round-tripped back above EUR 50/MWh, a 3.49% Monday gain driven by renewed Gulf shipping-risk sentiment rather than any European storage shortfall; German and French storage were both comfortably above 40% and 50% respectively that same week. The pattern recurs across the war: a Hormuz headline, whether a drone strike, an escort-capacity constraint, or a stalled LNG restart, reads in Doha and Rotterdam as a shipping story but lands in Amsterdam as a pricing one, adding a Gulf-risk premium to TTF that has little to do with how much gas Europe actually holds in storage.