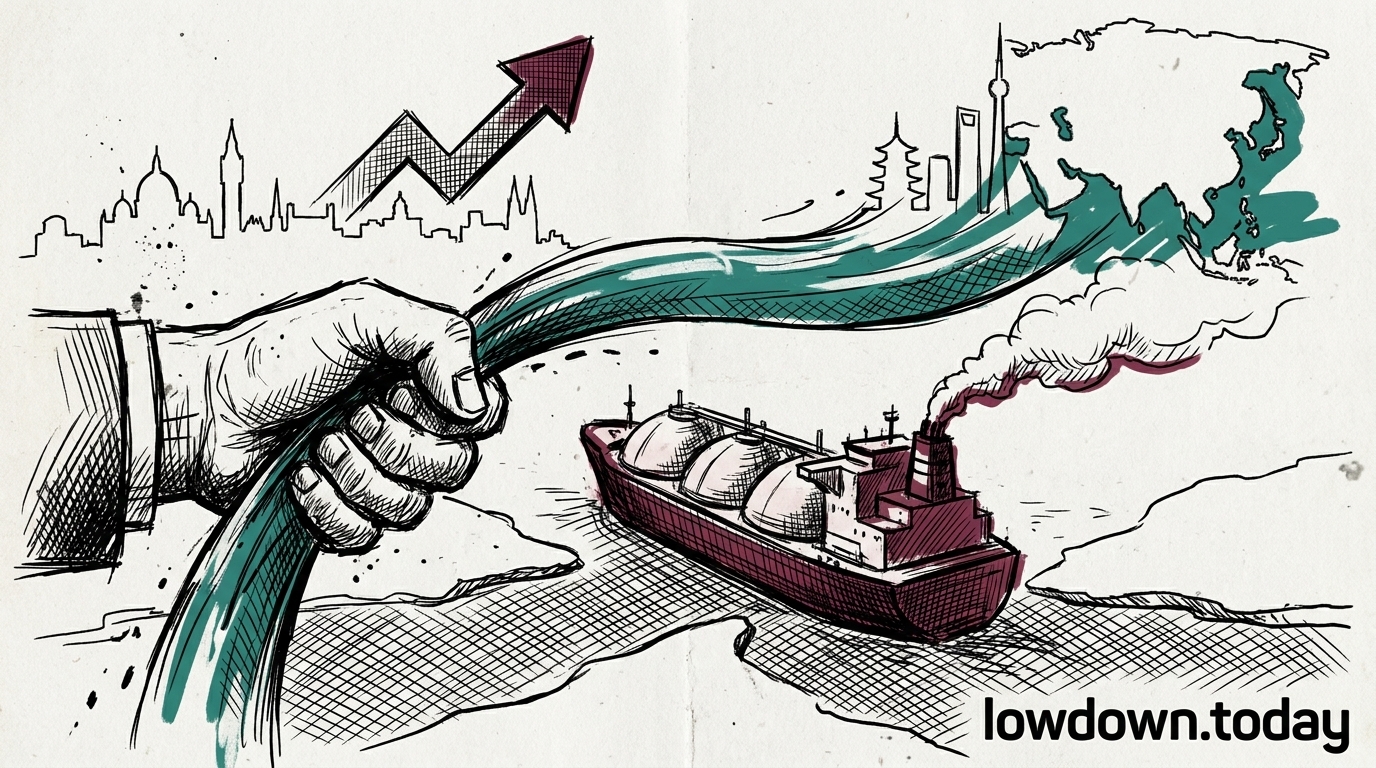

Following the 7 July strike on the Al Rekayyat, QatarEnergy CEO Saad al-Kaabi kept Ras Laffan output at a minimum, cut the number of vessels scheduled to dock, and extended force majeure notices to some Asian buyers into August, reversing the late-June guidance that the company would reach 50% of capacity within a month.

Qatar has withdrawn expected LNG volume rather than merely pausing, removing the marginal cargo Europe leans on during injection season.