EU Regulation 833/2014

EU's foundational Russia sanctions law; also bars European refiners from buying Iranian crude.

Last refreshed: 6 July 2026 · Appears in 1 active topic

Why does GL X's Iran oil relief leave European refiners completely shut out?

Timeline for EU Regulation 833/2014

Mentioned in: Diesel crack and Hormuz premium stack

European Oil MarketsRussia's diesel ban sets a record crack

European Oil MarketsMentioned in: OFAC cuts the Iranian-oil waiver short

European Oil MarketsContinued barring discounted Russian and Iranian diesel from the European pool

European Oil Markets: Diesel cracks hold as crude sells offBarred EU buyers from Russian and Iranian diesel

European Oil Markets: Diesel crack near $46 stays bidWhy can European refiners not buy Iranian oil even after General License X?

What does EU Regulation 833/2014 ban?

How many times has EU Regulation 833/2014 been amended?

Background

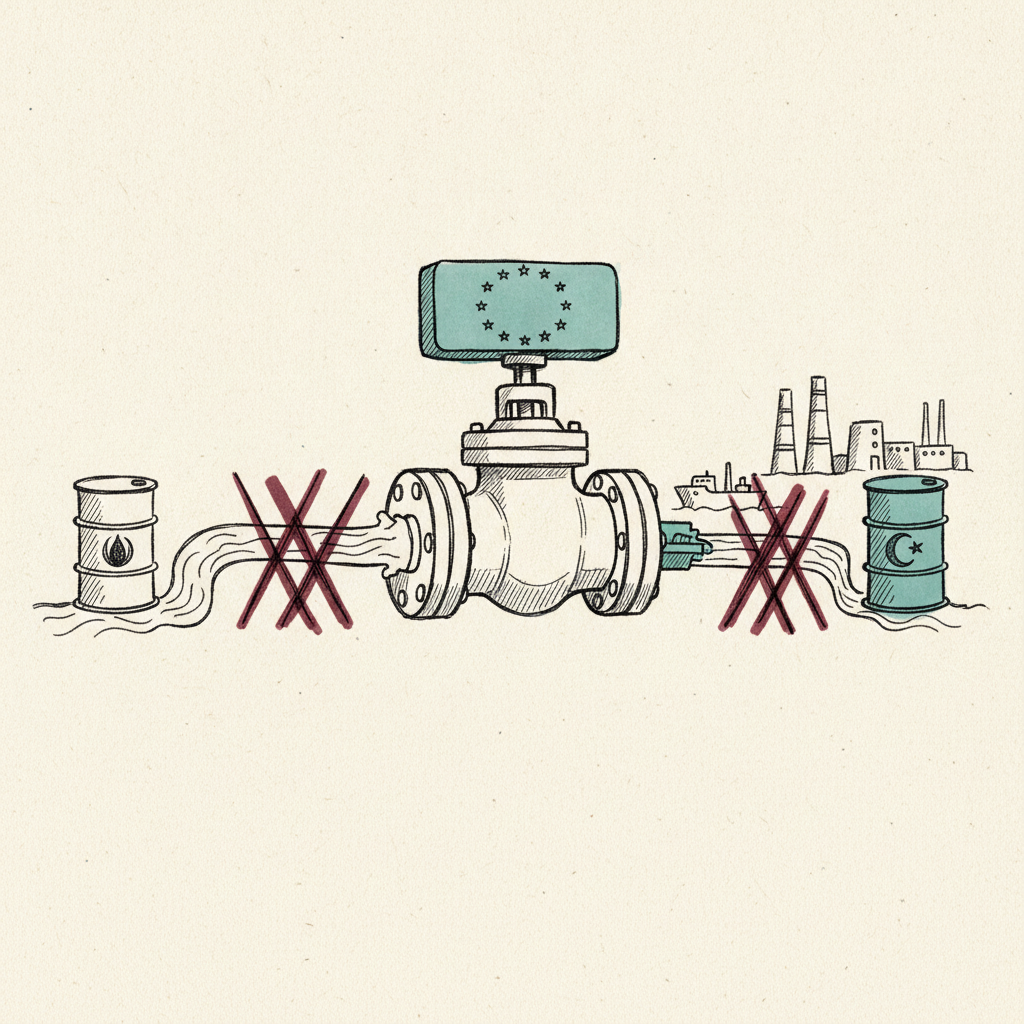

EU Council Regulation 833/2014 is the European Union's foundational Russia sanctions instrument, first adopted in July 2014 following Russia's annexation of Crimea and since amended through more than 20 successive packages. It prohibits EU-registered entities from importing Russian seaborne crude oil and petroleum products, underpins the G7 oil price cap by restricting the use of EU shipping, insurance and financing for Russian crude sold above the cap ceiling, and — critically for energy markets — also bars European refiners from sourcing Iranian crude, making it operationally distinct from parallel US sanctions administered by OFAC's General Licence regime.

The regulation's Iranian crude prohibition became the decisive market constraint on 22 June when OFAC issued General Licence X, authorising Iranian crude production, sale and shipping through 21 August. The announcement drove Brent towards $73, pricing a global supply loosening that European refiners cannot legally access. North-West European and Mediterranean desks cannot lift a single Iranian barrel regardless of OFAC policy; the flat-price softness structurally widens the ICE Gasoil crack against Brent because NWE/Med refining margins cannot benefit from cheaper Iranian feedstock .

The same bar keeps the European Diesel Crack itself elevated. Product-wire reporting on 3 July showed the crack holding near $46 even as outright crude sold off, with ARA independent gasoil stocks essentially flat near 13.5 million barrels . The margin holds on a rule rather than a fresh squeeze: because 833/2014 bars discounted Russian and Iranian diesel from the EU pool, the barrels that could compress the crack cannot legally reach it, so refiners keep earning an above-average margin regardless of where crude trades.

833/2014 enforces the G7 price cap by prohibiting EU shipping, insurance and financing for Russian crude traded above the cap price. Each successive package has widened vessel-tracking obligations and extended the shadow-fleet reporting requirements that are the principal tool for cap enforcement. The 21st package, adopted in 2025, further tightened evasion provisions and added new asset-freeze designations.